Probably the simplest menu pricing method is to go to a competitor’s food service operation, take the menu away, and copy the prices. Copying competitors’ menu prices is, however, a dangerous practice as conditions in any two types of food service operations are invariably different.

To determine food and beverage prices, however, a variety of factors should be considered, such as type of restaurant, meal occasion, style and level of service, competition, customer mix, and profit objective (Miller, 1980). Menu pricing procedures often rely on some form of cost-plus pricing technique.

For example, a restaurateur may establish a target food cost percentage of 44% of food sales revenue as an operating goal. This percentage is subsequently converted to a multiplier by taking the reciprocal of the percentage (Orkin, 1978). Thus, the multiplier equals:

1 / 0.44 = 4

This will multiply raw food cost by three to derive the price of a menu item. Instead of taking raw food cost, to multiply by an established pricing factor, it is also possible to use prime costs. This prime cost includes direct labor (labor involved in the actual preparation of the food item) and raw food cost.

Menu profitability, however, requires an absolute cash differential rather than a functional percentage relationship between cost and revenue. Thus, a menu item may have a preferable food-cost margin, but still make a lesser contribution to overhead expenses and net profit than another (similar popular) menu item (Table 1).

Table 1

| Starter | Soup | Carpaccio |

| Food Cost | $2.55 | $3.95 |

| Labor Cost | $2.05 | $2.15 |

| Prime Cost | $3.90 | $4.65 |

| Selling Price | $4.95 | $5.75 |

| Food /Cost Ratio | 51% | 57% |

| Prime/Cost Ratio | 74% | 78% |

| Contribution Margin | $2.35 | $3.05 |

| Table 1 Difference in food-cost ratio versus variation |

Another approach is to use a (differential) gross profit margin, for which the basic formula is:

Food/Beverage Cost per Portion + Gross Profit = Selling Price

Where the amount of profit contribution is set uniformly across all guests, hospitality firms may use: (Sales – Food Cost) / Number of Guests = Average Gross Profit

Where food costs are added to average gross profit to arrive at the menu item’s price. This variation of gross margin pricing is particularly suitable for establishments where customer counts are predetermined (e.g. in a hospital foodservice). It establishes lower prices for more expensive items and vice versa

One way to develop individual prices for dishes, meals and drinks, is what may be described as a ‘multi-stage approach’ which comprises of a number of distinct steps commencing with the estimated sales for a period and ending with individual food and beverage selling prices, as

illustrated in Figure 1 (Harris and Hazzard, 1992).

The initial stage includes the determination of the annual sales and average gross margin percentages that will provide a desired return on capital employed. The second stage requires the estimation of departmental sales mix with anticipated gross margin percentages.

Stage three comprises a further differentiation into departmental menu sales mix estimates. The last stage consists of estimating individual food and drink items as well as establishing selling prices.

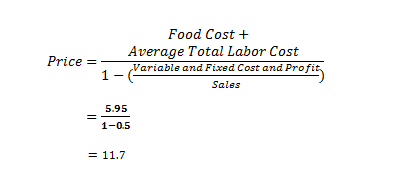

Yet another method to set menu prices is via the actual pricing method, which can also be used ‘backwards’ (i.e. the base price method) to meet the market or going price. The method includes the establishment of food cost and total labor cost as well as the determination of variable cost, fixed cost and profit as a percentage of sales.

For example, when raw food cost is $2.80, average total labor cost is $3.15, sales is $2,100,000, (the remaining) variable cost is $370,000, fixed cost is $480,000 and profit is 20% of $1,000,000 total assets employed (e.g. $200,000), the selling price equals

There is no question that a well-designed, properly priced menu is invaluable to restaurant operators having to succeed in an increasingly competitive environment (Hayes and Huffman, 1985). Due to its nature, the hotel and catering industry experiences a relatively high degree of product and service interrelationship.

For example, on the one hand an à la carte menu contains a number of courses which are interdependent in so much as they constitute a complete meal. The meal, on the other hand, cannot be seen in isolation, as a restaurant itself can be an interdependent component of a hotel as it forms part of the total service offering to a guest.

Therefore, hotel and tourism managers should be aware of the interdependence of departments and, thus, the pricing of accommodation, food and beverages should on no account be determined independently, but should represent a total business pricing effort (Rogers, 1976).